France’s economy is struggling to keep its head above water. France remains mired in sluggish activity as inflation and interest rates rise. Gross Domestic Product (GDP) growth is projected to increase by 0.9% in 2023. But the figure is largely the result of catch-up: quarterly activity has been at zero in three out of four quarters. And the next six months don’t look miraculous either. In its economic update released this Wednesday, INSEE expects GDP growth of… 0.2% for the first two quarters of 2024.

In fact, the organization did not change its forecast compared to December. “We should expect a very moderate recovery,” Confirmed Dorian Raucher, the new head of the economic department, during a meeting with reporters.

” The French economy has been stable over the past six months. For the first half of 2024, We can expect a timid resumption of activity “, he added.

For its part, the government is still counting on GDP growth of 1.4% in 2024. But this bet is now less and less credible in the eyes of most economists.

For its part, the OECD last Monday downgraded its projection by 0.2 points: 0.6% compared with 0.8% in November. The executive is expected to revise its growth numbers soon. And for good reason, in the euro zone, the drivers of activity are steady.

“Punished by inflationary shocks and fiscal tightening, activity has since stalled, with five consecutive quarters of nearly zero growth”.The authors suggest an economic point.

Stay at half mast

On the investment front, bad news is piling up. After a gloomy 2023, INSEE predicts no improvement in the coming months. Some leading indicators, such as the business climate in wholesale trade or planned investment in services, have continued to decline indefinitely for two years.

“Business investment appears to have stalled due to the tightening of monetary policy and the wait-and-see attitude of leaders in terms of demand”.Dorian underscores the doucher.

“Till the beginning of 2023, there was resistance in business investment. But now it’s unpleasant.”.

On the household side, the decline at the end of 2023 (-1.4% in the last quarter) should continue at least until the first half of 2024. “The main channel through which the effects of monetary policy pass is household investment”., explains the economic forecaster. As a result, the construction and real estate sectors are likely to suffer for a long time to come. “Overall, real estate developers are very pessimistic in surveys”. Given the propagation time for the effects of monetary policy on the economy estimated at between 12 and 18 months, the horizon for construction players risks remaining bleak for longer.

The industry is still in the red

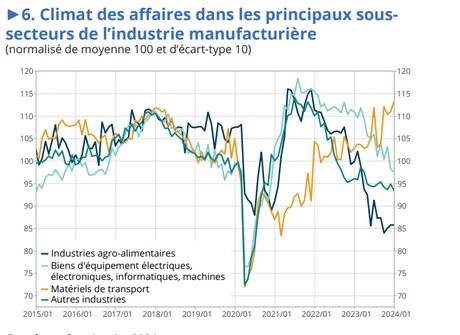

In the industry, the indicators are also disappointing. The business climate in key branches of the manufacturing industry has been in free fall since early 2021. The resumption of the economy during the post-pandemic deconfinement led to a recovery in the drivers of French industry. But beyond this basic effect, “Made in France” is still struggling.

Except for transport equipment manufacturing, confidence indices are well below their long-term averages. “There is a strong disparity between the transport industry and the food industry”, notes Dorian Daucher. But the overall trend of the curves is rather unfavorable.

Inflation will be 2.5% in June.

On the inflation front, inflation may ease to 2.5% by next June. After reaching 3.7% in December, the General Price Index fell to 3.1% at the end of January. “Food was the main contributor to inflation between September 2022 and September 2023”Summary Clement Bortoli, VsHead of Economic Summary Section.

“Now it is services that should mainly contribute to inflation with wage dynamics”He continued.

In the private sector, “Wages are slowing slightly (after an annual average of +4.5% in 2023), but remain fairly dynamic as negotiations are based on past inflation. Mid-year average salary increase per capita will be +2.6% »Details on gallery, Dorian Raucher.

On the public sector side, “The average salary per capita has developed at the same pace, but slightly lower than the private sector (+4.0% in 2023), especially due to clear measures in favor of teachers and the revaluation of index points on July 1. , 2023. In early 2024, new measures were implemented and growth will be slightly lower than that of the private sector. Average salary per capita will increase by +1.9% in mid-year ».

Core inflation should reach 2% in June

In terms of underlying inflation, it may stabilize at 2%. As a reminder, this index “Excludes the most volatile elements, i.e. prices subject to state intervention (electricity, tobacco, etc.), petroleum products or fresh produce”.

Core inflation “Overall reflects inflationary pressures better than the index, as it is less disturbed by external events”Remembers Dorian Raucher.

“ Between now and June, underlying inflation should decline significantly, as should headline inflation (2.1% expected for underlying inflation versus 2.6% for headline inflation). This reduction is mainly explained by the expected decline in inflation of food products (excluding expenditure) as well as manufactured products. », he adds.

This price development is close to the target set by the European Central Bank (ECB) at 2%. But euro zone central bankers appear in no rush to cut rates. During her latest interventions, the president of the ECB, Christine Lagarde, was particularly cautious. However, activity in the euro zone has already dipped through 2023 due to the effects of monetary policy tightening. And the aftershocks of a rate hike could still reverberate for several months, especially on the stuck monetary union economy. Poor growth.

Resume usage

This disinflation will breathe new life into the purchasing power of households and employees. Struck by a surge in inflation, many French have had to cut their consumer spending to make ends meet for nearly two years. For the first half of the year, INSEE takes it into account “Consumption will be the primary driver of activity”, argues Dorian Raucher. French household confidence rebounded at the end of 2023. But its level remained 10 points this side Its long-term average (100).

Which means that a large proportion of French people with the highest propensity to consume will continue to tighten their belts. And wealthy families can continue to save. The savings rate (around 17%) is on average higher than its 2019 level. But it will be brought “ to stabilize », predicts Dorian Raucher.

“Income from assets tends to increase the ability to save. It is the wealthiest households, i.e. the bottom quartile, who have continued to save after the health crisis. Other households, on the other hand, have returned to more normal levels of savings”.

Suffice it to say that the saving lever for increasing consumption remains relatively limited.